NBFC and Fintech

A full-stack

digital lending solution

for NBFCs and FintechsCreate escrow accounts and operate through APIs for loan disbursements, repayments and co-lending, in compliance with RBI’s

digital lending guidelines

.Secure

Scalable

Compliant

Your Payments Partner

India's 1st Fintech platform to enable disbursal of loans and insurance claim settlements

600000

Merchants

80

Processed annually

600

Bank accounts served

Our tailored solution enables NBFCs and their partner LSPs to scale their

digital lending business

Term Loans for individuals & businesses

Buy Now Pay Later

Co-lending

InvoiceDiscounting

Supply Chain Finance

Credit Line Infrastructure

Managed Escrow Solution for NBFCs and LSPs

NBFCs

Perks

Get fully managed escrow set-up with multiple banking partners

Get access to detailed and customized MIS report

Enable LSPs to manage complete disbursement & repayment cycle on Cashfree Payment's Dashboard or use our APIs

Get access to loans, disbursed statements and balance for each LSP on your escrow

LSPs

Perks

Manage multiple NBFC relationships through our solution

Ensure visibility and ability to manage the loan cycle for your customer base

Get access to dashboard and APIs for disbursement and repayment on NBFC escrow

Get access to detailed and customized MIS report for loans originated and repaid for your customers

Make

instant loan disbursals

directly from your current or escrow accounts with Cashfree Payments’ APIsContact Sales

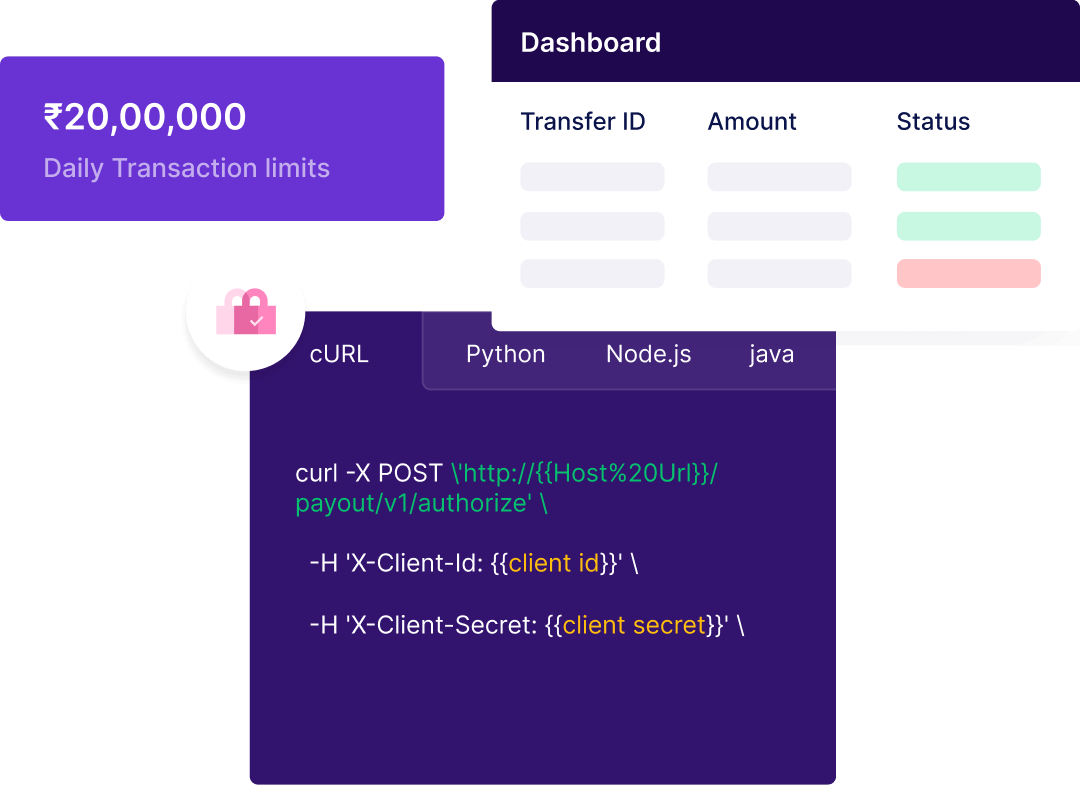

Disburse loans from multiple accounts

Connect multiple existing current or escrow accounts and switch between them for payout.

Enable co-lending use cases with NBFC escrow

Create flexible virtual accounts and use APIs on your NBFC escrow account to enable co-lending use case.

Reduce dependency on a single bank

Switch between connected bank accounts. Avoid any unforeseen exigencies of bank downtimes with multi-bank support.

Get support at lightning speed

Get dedicated support to set up multiple party escrows or trustee escrows for disbursal.

Banking Partners:

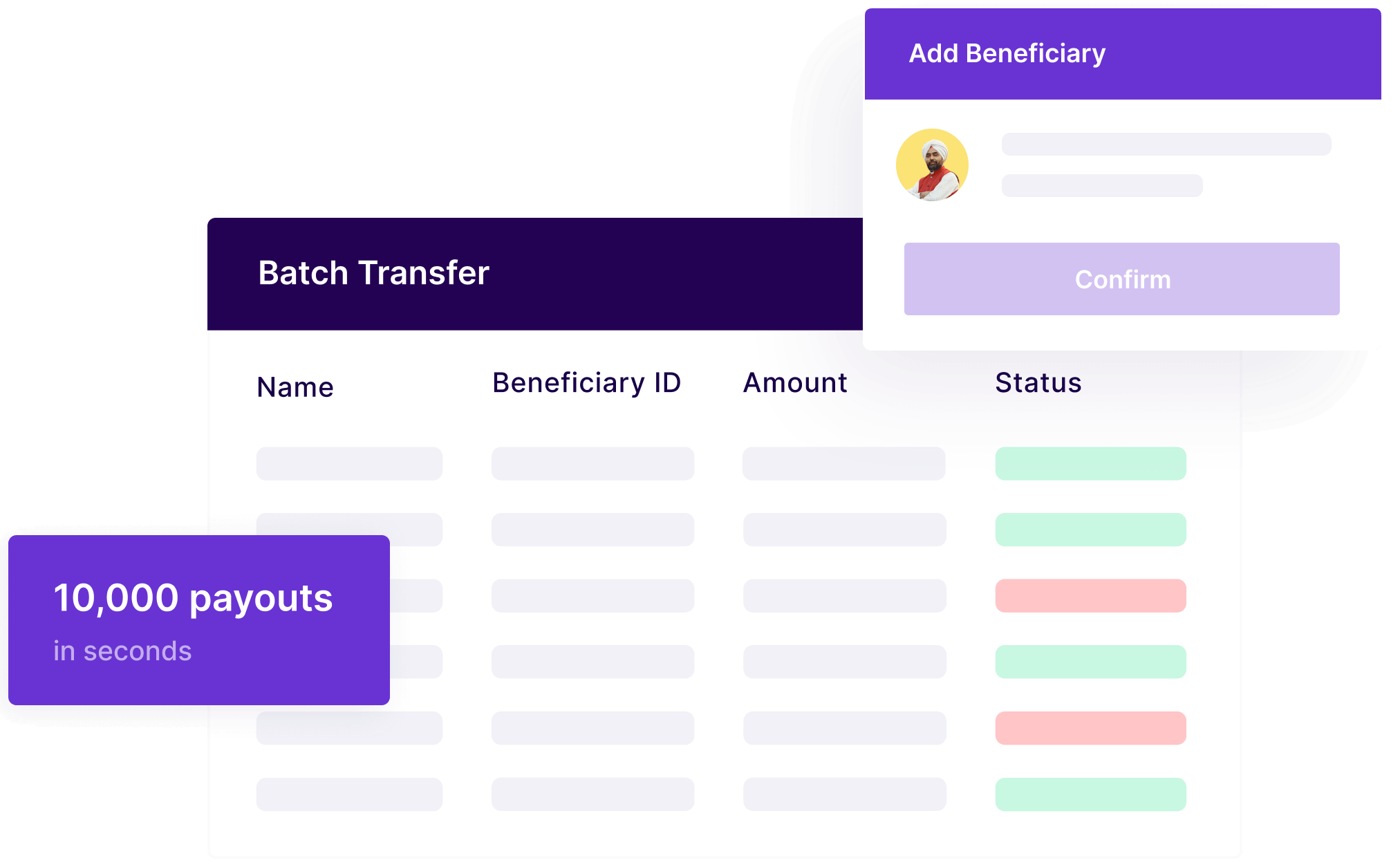

Powerful merchant dashboard

Disburse loans

and make other payments directly from your connected business accountAdd borrowers and make up to 10,000 payouts in seconds from NBFC escrow

Track transfer status and reasons for failure in real time

Generate custom reports for deeper analysis

Streamline loan disbursals with direct Payouts integration

Cashfree Payments helped Northern Arc provide instant consumer &

business loan disbursals

and effectiveloan solutions

to all, by simply integrating direct Payouts in their Loan Origination System, eSthenos. With this, Northern Arc could:Verify borrower bank accounts before disbursing consumer & business loans.

Save man hours by disbursing thousands of consumer & business loans automatically.

Automatically reconcile failed transfers and reversals.

Effortlessly collect payments while adhering to RBI's digital lending guidelines

Collections and reconciliation

Receive loan repayment directly into your NBFC account. Instant reconciliation & same day settlement.

Recurring payments

Set up recurring mandates for repayment. Collect recurring payments via debit cards and Net Banking using NACH E-mandate & UPI Autopay using TPV flow.

Split payments

Split repayment received and settle into co-lenders’ accounts directly.

Recommended for

co-lending use cases

Real-time reports

Leverage repayment reports and statements data for accounting compliance.

Collections and reconciliation

Collections and reconciliation

Receive loan repayment directly into your NBFC account. Instant reconciliation & same day settlement.

Recurring payments

Recurring payments

Set up recurring mandates for repayment. Collect recurring payments via debit cards and Net Banking using NACH E-mandate & UPI Autopay using TPV flow.

Split payments

Split payments

Split repayment received and settle into co-lenders’ accounts directly.

Recommended for

co-lending use casesReal-time reports

Real-time reports

Leverage repayment reports and statements data for accounting compliance.

Verify Borrower identity

Onboard borrowers with ease using our 360° Verification Suite

[For individuals and businesses] Provide an easy onboarding experience for your users by verifying their bank accounts & UPI IDs, PAN, Aadhaar and GSTIN using our APIs and dashboard.

Revolutionize lending with Cashfree Payment's solution for NBFCs & LSPs

With

Cashfree Payments

With

Other Platforms

Time to go live

Easy to integrate and go-live in 3 weeks

Difficult to integrate. Delayed onboarding

Product Suite for different payment needs

One-stop solution. Low code APIs & dashboard access for easy loan disbursement & collections

Fragmented and siloed products. Multiple vendor integrations required

Ease of service

Dedicated support in escrow creation

Multiple points of contact

Dashboard

Connect multiple escrow/current accounts with single dashboard

Multiple dashboards, and limited view

Risk Mitigation

Real time risk management with powerful risk engine

Have better control on funds movement, take action, and minimize risk with real-time updates.

Set transaction limits

API level security checks

Fraud detection

Ready to get started?

Get your business festive ready today with 0% payment gateway fees,on sales up to ₹20L*. Start now by creating your account and unlock your growth journey.

Go Live in Minutes

Dedicated account manager

Next-Day Settlement