Use cases

The following are key use cases for reverse penny drop verification across regulated financial sectors:- Banks: Verify bank account ownership for savings, current, and business accounts during customer onboarding. Enable instant account verification for credit services and loan applications. Meet RBI compliance requirements for account validation.

- NBFCs and fintechs: Complete bank account verification for personal loans, credit cards, BNPL services, and digital lending platforms. Support fraud prevention through real-time account ownership validation.

- Investment and wealth management: Verify bank accounts for Demat account opening, mutual fund investments, and trading account setups. Comply with SEBI regulations for investor account verification.

- Insurance companies: Validate bank accounts for policy premium payments and claims processing. Authenticate policyholder bank details for direct settlement processes.

Key benefits

The following features help you deliver a reliable, efficient, and user-friendly verification experience:- Instant verification results: Complete bank account verification within 2-5 minutes compared to traditional methods that take days. Receive real-time confirmation of account ownership and details.

- Customer-controlled process: Enable customers to verify their accounts using any UPI app of their choice without manually entering bank account numbers or IFSC codes. Provide multiple payment options including QR codes and UPI intent links for seamless verification.

- Enhanced security and fraud prevention: Validate active account ownership through customer-initiated payments. Reduce risks associated with fake or dormant bank accounts and minimise chargeback risks.

- Regulatory compliance: Meet RBI guidelines and banking regulations for account verification. Ensure compliance with KYC requirements across financial sectors.

- Seamless integration: Integrate with existing systems using developer-friendly APIs. Support both webhook and polling methods for status monitoring.

- Active account confirmation: Unlike traditional methods that only match IFSC codes, reverse penny drop verifies that accounts are actively receiving payments and operational.

- Cost-effective solution: Eliminate manual verification processes and reduce operational costs. Automatic refund processing within 24-48 hours.

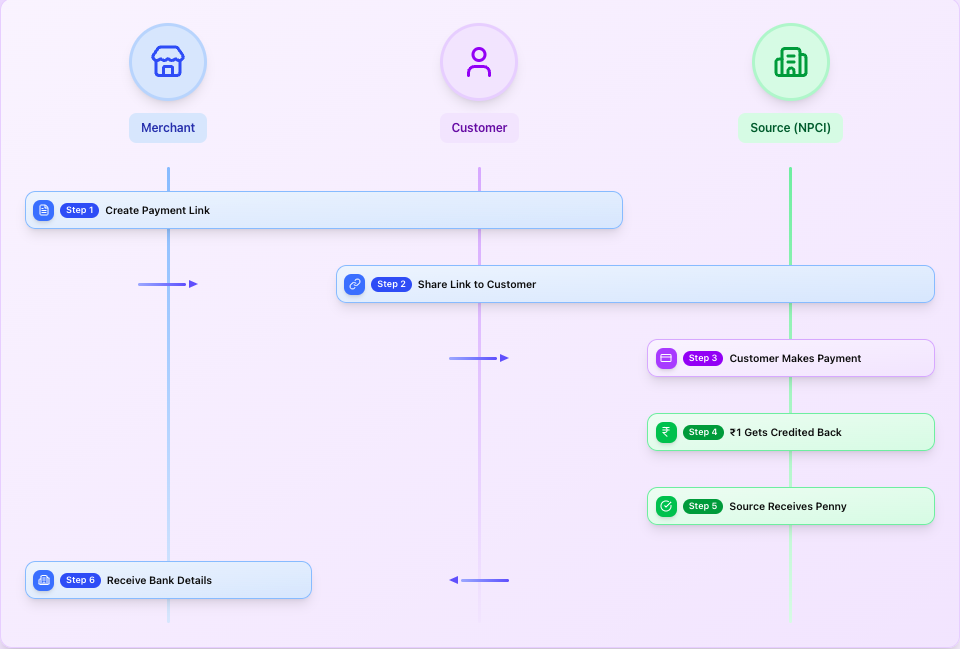

Verification process

The reverse penny drop verification follows a simple, secure workflow:Create Payment Link

redirect_url parameter to specify where the user should be redirected after completing the payment on the webpage. If not provided, users will be redirected to www.google.com by default.Share Link to Customer

Customer makes payment

₹1 gets credited back

Verification confirmation

Receive bank details

- CREATED: The request is created, but no payment has been made yet.

- SUCCESS: A successful transaction returns all fields in the response.

- FAILURE: The payment attempt failed for an unspecified reason.

- EXPIRED: The link in the create request call expires after 10 minutes if no payment is made.

url field that contains a link to the webpage with the generated UPI link and QR code. To enable this field, fill out the Support Form or contact your account manager.

FAQs

What is reverse penny drop verification?

What is reverse penny drop verification?

What are the benefits of using reverse penny drop for businesses?

What are the benefits of using reverse penny drop for businesses?

What are the benefits of using reverse penny drop for users?

What are the benefits of using reverse penny drop for users?

Can all lines of business use reverse penny drop?

Can all lines of business use reverse penny drop?

- 7322: NBFC (debt collecting agencies)

- 6012: Mutual Funds (financial institutions - merchandise and services)

- 6211: Security Brokers/Dealers (merchants that buy, sell, and broker securities, stocks, bonds, commodities, and mutual funds)

- 6300: Insurance Sales, Underwriting, and Premiums

How long is the reverse penny drop link valid?

How long is the reverse penny drop link valid?

Can I redirect users to a custom URL after payment completion?

Can I redirect users to a custom URL after payment completion?

redirect_url parameter when creating the reverse penny drop request. This URL specifies where the user should be redirected after completing the payment on the webpage. If you do not provide a redirect_url, users will be automatically redirected to www.google.com by default.What information do I receive after successful verification?

What information do I receive after successful verification?

- Bank account number

- IFSC code

- Virtual Payment Address (VPA) used for the transaction

- Verification status and transaction details

- URL link to the webpage containing the generated UPI link and QR code for the reverse penny drop request

How long does the refund process take?

How long does the refund process take?

What happens if the verification fails?

What happens if the verification fails?

FAILURE status. Common reasons for failure include:- Network connectivity issues during payment

- Insufficient balance in the customer’s account

- Payment timeout or cancellation by the user

- Technical issues with the UPI infrastructure

Can users verify accounts from any bank?

Can users verify accounts from any bank?

Is there a limit on the number of verification attempts?

Is there a limit on the number of verification attempts?

How do I handle the verification status in my application?

How do I handle the verification status in my application?

CREATED: Request created but payment not yet madeSUCCESS: Verification completed successfullyFAILURE: Verification attempt failedEXPIRED: Link expired (10 minutes) without payment

What security measures are in place to protect user data?

What security measures are in place to protect user data?

- All API communications use HTTPS encryption

- Bank account information is transmitted securely through UPI rails

- Data is stored with industry-standard encryption

- Access to verification data is logged and monitored

- Compliance with PCI DSS and other security standards